Weekly Market Recap (Feb 16th)

“Higher for Longer” is back?

This week’s main theme was a resurgence of the “higher for longer” policy rates narrative as CPI and PPI inflation data came in hotter than expected. Further, the preliminary Michigan survey data for February confirmed that the disinflation process will not be easy from here. However, equities saw a modest dip as investors rotated out of the Tech stocks and other winners into small-cap and other underperformers. For the week, the S&P 500 and NASDAQ fell 0.4% and 1.5% respectively, while equal weight S&P 500 and Russell 2000 rose 0.6% and 0.5%, respectively. So the bears who are waiting for a bigger dip were disappointed as investors are optimistic that the deflationary process has been delayed but not derailed.

Let’s recap what happened this week

A hot CPI data print on Tuesday caught the risk markets by surprise as the S&P 500 fell 1.4% on the day, slipping under the 5,000 level. However, that move was short-lived as the dip was bought quickly sending the S&P 500 index to new all-time highs. Softer-than-expected US retail sales print threw a complicated message on the growth front, but also gave fuel to the narrative that the disinflation process is going to be bumpy but the trend is still downward. The small cap index Russell 2000 also reached a YTD high yesterday after seeing its worst fall since 2022 during the CPI rout.

This morning, the market got another reminder of the possible re-acceleration of inflation as the January US PPI came in higher than expected. Together with the CPI print from earlier in the week, the significant beats in Jan PPI confirmed expectations for a solid core PCE (to be released on Feb 29). Note that PCE is also the Fed’s preferred inflation gauge and current data suggests that the Fed will remain hawkish or rather patient when it comes to cutting Fed Funds rates. Sharing an interesting thread that pushes back on the standard explanations for why US disinflation will continue.

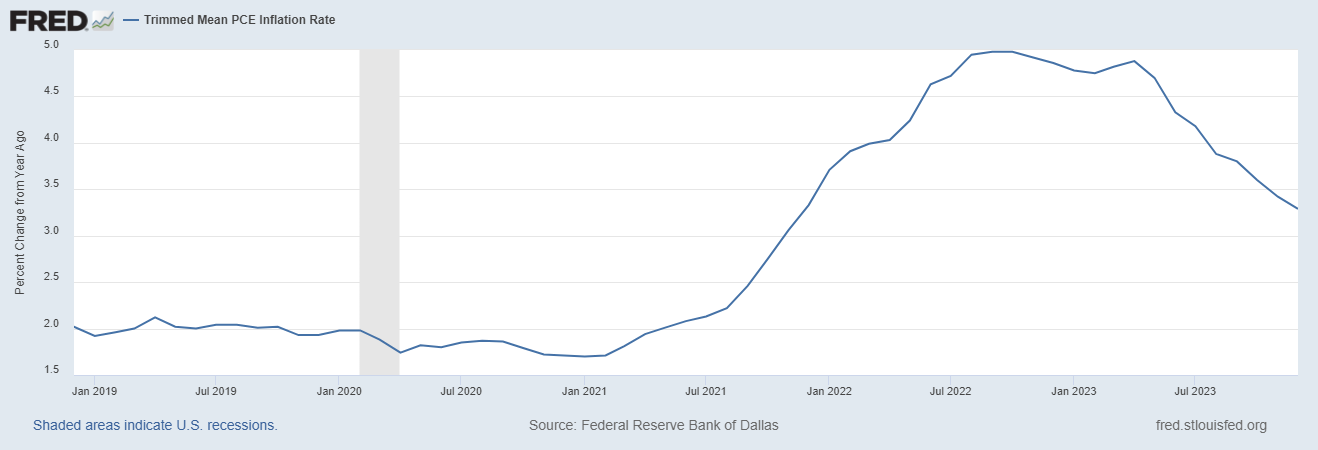

This morning, Atlanta Fed’s President Bostic noted he was modestly surprised by the data "but not in a big way." He foresees more declines in inflation but reiterated the path back to 2% could be uneven. Bostic said that he needs more data to convince him inflation pressures are truly falling, but also mentioned that "My outlook is to start the normalization, start returning our policy stance to a more neutral stance in the summertime," in a CNBC interview. He also cited the Dallas Fed's trimmed-mean PCE price statistic, which posted a 2.6% annualized increase in December, identical to its reading over the past six months, as a reason to be not too optimistic that inflation goals have been achieved. The link to his speech from yesterday is worth a read.

Impact on Rates Market

While risk markets have been quite unfazed by the hotter inflation data, the rates market has repriced significantly this week.

In the short end, the number of cuts priced in for 2024 has decreased to 3.5 cuts (88bps) as of Feb 16th vs. 6-7 cuts priced at the beginning of the year. Meanwhile, the first cut has been pushed to June from May earlier in the week.

The yields on the 2Y and 10Y notes are also trading at 4.65% (+18bps) and 4.29% (+10bps), respectively.

Earnings Season Update

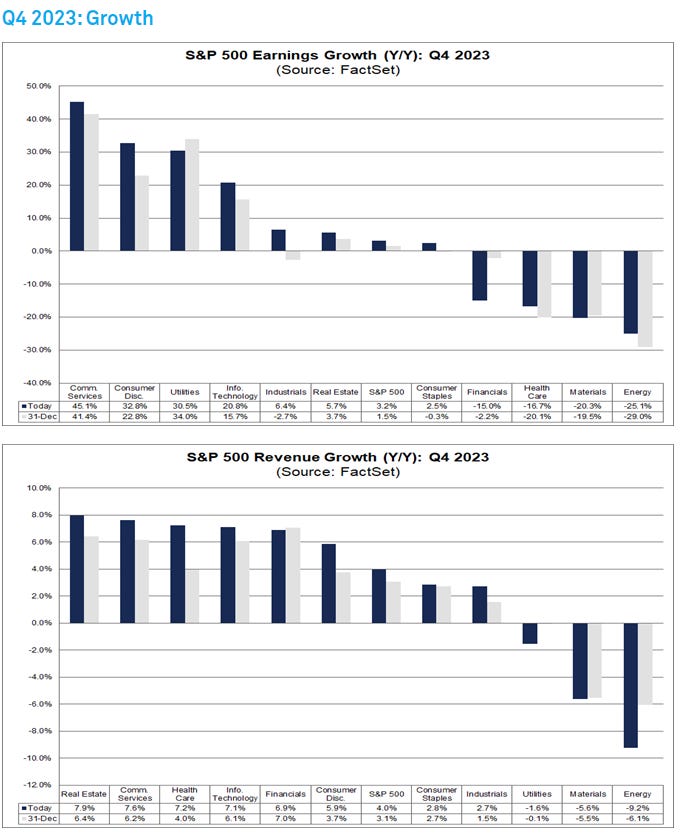

Overall, 79% of the companies in the S&P 500 have reported actual results for Q4 2023 to date. Key takeaways from the season are:

Of these companies, 75% have reported actual EPS above estimates, which is below the 5-year average of 77% but above the 10-year average of 74%. In aggregate, companies are reporting earnings that are 3.9% above estimates, which is below the 5-year average of 8.5% and the 10-year average of 6.7%.

The index's fourth-quarter earnings have improved, with a current blended growth rate of 3.2%, up from 2.8% last week and 1.5% at the quarter's end.

Looking forward, analysts are optimistic, projecting earnings growth of 3.9% for Q1 2024 and 9.0% for Q2 2024, with a 10.9% growth expected for the entire year of 2024. However, this optimism is tempered by a relatively high forward 12-month P/E ratio of 20.4, which is above both the 5-year and 10-year averages, suggesting that stocks might be valued more expensively compared to historical norms. This could imply investor confidence in future growth or a potential overvaluation in the market.

Source: Factset

Chinese stocks outperform US markets

Chinese ETFs rose this week after remaining closed for the Lunar New Year holidays. The price action was supported by a Bloomberg article noting a resurgence in travel during China's Lunar New Year holiday, signaling a possible rebound in consumer spending in the struggling economy. Official data shows over 61 million rail trips in the holiday's first six days, the highest in five years and a 61% increase from the same period in 2023, highlighting a shift in consumer behavior. Concurrently, the WSJ reported that the Chinese government is poised to significantly expand its real estate involvement, potentially acquiring distressed projects or building more subsidized housing, as part of President Xi Jinping's initiative to increase state control over the sector.

Major events for next week

NVDA earnings on Feb 21st - The expectations are probably much higher this time around compared to the last two quarterly earnings reports as the stock has rallied 48% since the last earnings release.

FOMC Minutes on Feb 21st

Other news:

Funds from Japan and China dumped record amounts of US stocks last year to mine double-digit returns BBG

Is the US power grid at risk, along with your home? BBG

How distressed debt brought a billionaire’s satellite empire crashing to earth FT

US investors in emerging markets switch to ETFs that exclude China FT

Pimco joins JPMorgan and State Street in quitting climate investor group FT

Text-to-studio quality short films are now a web link away: NYT

Some budget-stressed small colleges have begun selling off some of their real estate holdings to get the bills paid NYT

UAW workers at Ford's Kentucky truck plant threaten strike next Friday RTRS

The BOJ is on track to end negative rates in the coming months- despite the economy's slip into recession RTRS

Fed's Barr says supervisors more aggressive, honing in on interest rate risk RTRS

The price cuts keep coming for America's EV-makers WSJ

Realtors are in crisis and homeowners could be the big winners WSJ

The impact of recent immigration on US economic output, productivity and wages: WSJ