Market Resurgence

Navigating the Rebound and Outlook Ahead

After a brief hiatus, the MarketMuse newsletter returns with fresh insights on the market dynamics.

Are Tech Stonks heading back to the moon 🚀?

US major indices have rebounded from their mid-April lows, fueled by signs of disinflation, easing geopolitical tensions (the Israel-Iran incidents were more symbolic than escalatory), a retreat from peak hawkishness by the Fed, and stronger-than-expected earnings, providing investors with some relief.

The NASDAQ index, just shy of its all-time highs, boasts an 8.8% YTD gain despite mixed results from the Mag 7 group. However, the landscape isn't entirely rosy. The post-earnings tumble in META shares, coupled with remarks from Drunkmiller on CNBC, underscore the potential near-term volatility in the AI sector. NVDA's upcoming earnings on May 23rd and heightened S&P 500 forward implied volatility suggest the market is bracing for significant moves. Similarly, PLTR’s decline post-earnings, despite exceeding forecasts and elevating guidance, signals a possible retreat in the AI trade.

Next leg higher for S&P 500

Since its recent trough on April 18th, the S&P 500 has rallied 4.4%, though it has slightly retracted from the 5200 level in today’s session. This pause, just ahead of upcoming inflation data (PPI on 05/14 and CPI on 05/15), seems healthy. An inflation report in line with expectations could temporarily boost stocks as markets cheer the dip in Treasury yields. Yet, signs of renewed disinflation could increase the odds of more fed fund rate cuts, bolstering stocks amid growth concerns.

Currently, the market anticipates a 42bp cut this year, with July seeing a 33% chance and September an 82% probability of rate cuts.

Risk/Reward on Treasuries

The US Treasury market was hit hard in recent months as the hot inflation data along with negative sentiment pushed yields to highs not seen since September 2023.

However, several factors now tilt the risk/reward balance in favor of Treasuries:

Inflation has likely peaked as evidenced by falling commodity prices (Bloomberg Commodity index below)

Real world prices appear to have peaked:

Real-world price indicators, such as the Manheim Used Car Index for April, suggest ongoing deflation in the auto sector.

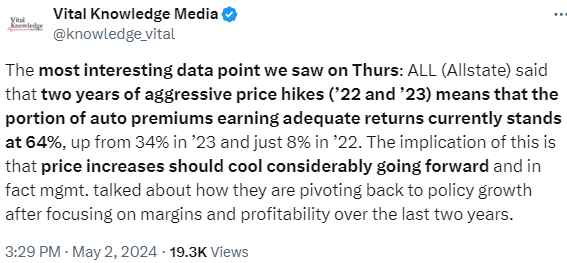

Auto insurance premiums have likely reached their peak.

Shelter inflation - most publicly traded housing rental firms show a deceleration in revenue and rental growth which is not yet reflected in CPI/PCE data.

Red flags from Q1 earnings and a softer-than-expected April jobs report highlight the risk on the growth front

Treasury auctions aren’t growing but the pace of QT is set to slow meaningfully

Most Fed speakers have a pretty high bar for another rate-hike

On the other hand, the US fiscal landscape is dominated by substantial deficits and a noticeable lack of political will for significant fiscal reforms. This suggests that the record-low Treasury yields of the previous decade are unlikely to recur under the current fiscal climate.