Jobs Report Reset the Course

All eyes on CPI and FOMC next week

The week began with US economic data indicating a cooling growth trend, as both the ISM manufacturing and JOLTS reports came in below expectations. However, the momentum shifted dramatically when the US nonfarm payrolls far exceeded expectations. The establishment survey revealed that the US economy added 272K jobs in May 2024, the highest in five months, compared to a downwardly revised 165K in April and significantly above the forecast of 185K. This figure also surpassed the average monthly gain of 232K over the past 12 months and 246K in the first four months of the year. Average hourly earnings accelerated to 0.4% MoM. However, these positive numbers were tempered by the more volatile Household survey, which showed the economy lost 408K jobs, and the unemployment rate rose to 4%.

Although the May Jobs report would keep the Fed on hold, the US job market may be a lot less vibrant according to this Bloomberg report. It suggests that payrolls might have grown about 60,000 less per month on average last year than the roughly 250,000 run-rate derived from the agency’s monthly employment report. The new figures, from the Quarterly Census of Employment and Wages, cover more than 95% of US jobs and are eventually used in annual revisions to the monthly data.

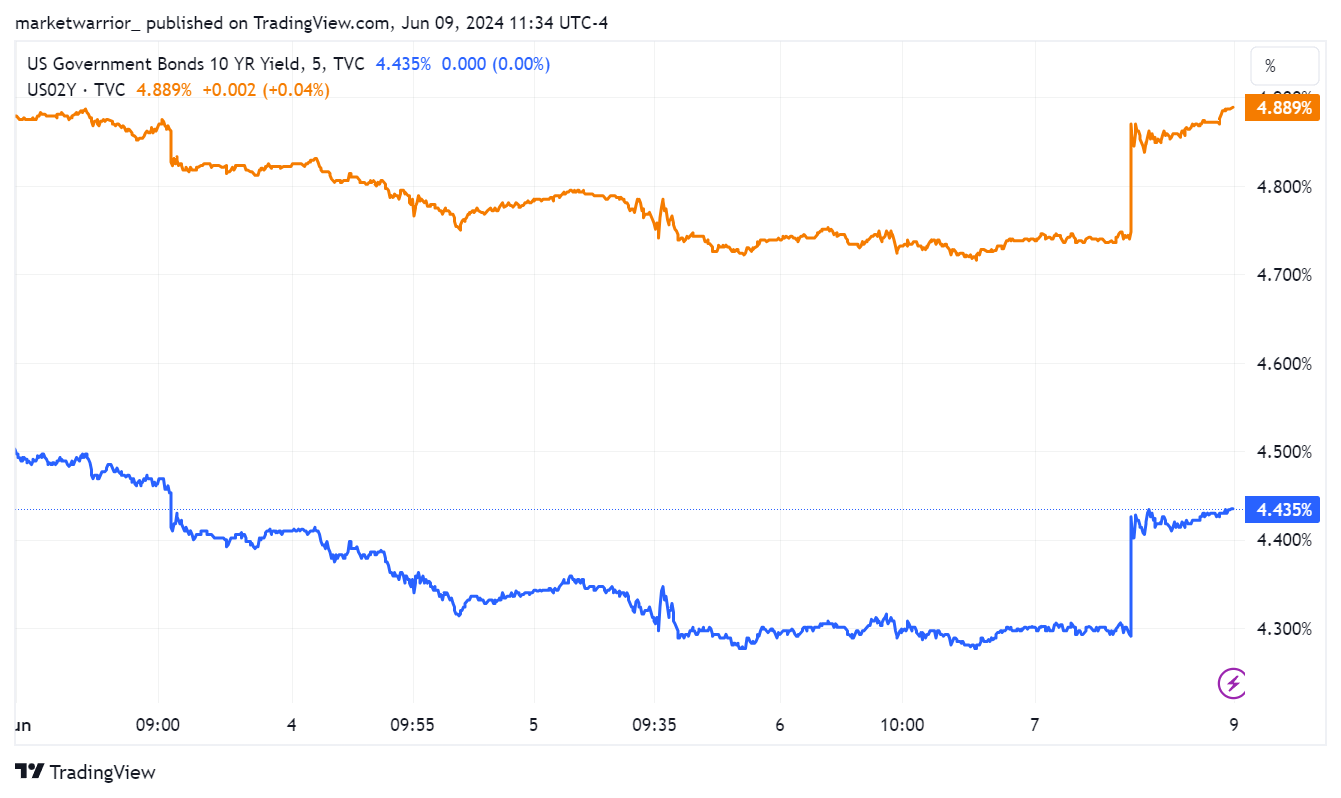

Treasury yields soared 10-15bps across the curve, led by the front-end, where US 2y yields climbed towards 4.90%, and 10y yields topped out near 4.44%. Positioning was stretched long US Treasuries before Friday’s US jobs data, which exacerbated the price action on the day. Fed's guidance on rate cuts next Wednesday is a key risk.

The expectations for the first Fed interest cut also shifted in a hawkish manner with the odds of a September cut declining to 50% compared to 75% on June 5th, with ~37bp (down from ~44bp on June 5th) worth of reductions priced in for the year.

Equities

Despite recent growth concerns, the S&P 500 and Nasdaq 100 managed to finish the week positively, overcoming an early selloff on Friday caused by higher US yields. The Nasdaq closed at 17,133 (+2.4% w/w), while the S&P 500 consolidated around 5,350 (+1.3% w/w). However, the equal-weighted S&P 500 index ETF declined by 0.7% w/w, and the small-cap Russell 2000 index fell by 2.1% w/w, making them the laggards.

Next Week’s Catalysts

Monday, 6/10

Apple WWDC keynote (1pm ET) - We expect Apple's WWDC keynote to focus on on-device AI capabilities and GenAI models. The presentation should differentiate the iPhone 16 with AI features, sparking an upgrade cycle starting in 2024. Note that AAPL has lagged Mag7 peers, so expectations remain high for AAPL to prove it will continue to be a major player in the AI conversation.

Tuesday, 6/11

Earnings: ORCL (night)

Wednesday, 6/12

US CPI for May (8:30am ET) - the street projects core CPI to slow to 3.5% y/y from 3.6% y/y in April, while headline inflation is expected to hold constant at 3.4% m/m. Market attention will be on any indications of a sequential slowdown in shelter inflation, as the Fed has long anticipated. Zillow rents have been rising at a pre-pandemic pace for some time, but now the new tenant rent index has softened along with general housing activity.

FOMC decision (2pm ET) - The focus will be on the dot plot and Summary of Economic Projections (SEP). When it comes to forward guidance, the Fed has made it clear that the bar for further hikes is very high. Keeping that in mind, the market widely anticipates the 2024 one moving down, reflecting two cuts this year instead of the prior three. A drop to just one cut would be seen as hawkish - though this is not the base case. The longer-run dot shouldn’t move up materially, stands at 2.6%. GDP estimates could have modest downside risk and the unemployment rate outlook could have slight upside risk given the May reading of 4%. The inflation forecast could remain unchanged given the cooldown in growth expected.

Earnings: AVGO, PLAY (night)

Thursday, 6/13

US PPI for May (8:30am ET)

BOJ decision (night)

Earnings: ADBE (night)